The Evolution of the 30 Year Mortgage: A Comprehensive Look at Trends and Insights

Related Articles: The Evolution of the 30 Year Mortgage: A Comprehensive Look at Trends and Insights

Introduction

With great pleasure, we will explore the intriguing topic related to The Evolution of the 30 Year Mortgage: A Comprehensive Look at Trends and Insights. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

The Evolution of the 30 Year Mortgage: A Comprehensive Look at Trends and Insights

The 30 year mortgage has been a cornerstone of the American dream for generations, providing a predictable and affordable path to homeownership. This long-term financing option offers a consistent monthly payment, allowing borrowers to budget effectively and build equity over time. However, the landscape of 30 year mortgages is constantly evolving, shaped by economic conditions, government policies, and changing consumer preferences. This comprehensive guide explores the historical trends, current dynamics, and future prospects of this essential financial instrument.

Historical Trends of the 30 Year Mortgage

The 30 year mortgage emerged in the early 20th century as a response to the growing demand for affordable housing. Prior to its introduction, home loans typically had much shorter terms, making homeownership inaccessible to many. The fixed-rate structure of the 30 year mortgage provided stability and predictability, making it an attractive option for families seeking long-term financial security.

1930s-1950s: The Rise of the 30 Year Mortgage

The Great Depression and World War II significantly impacted the housing market, leading to a decline in homeownership. In response, the federal government introduced programs like the Federal Housing Administration (FHA) and the Veterans Administration (VA) to stimulate the housing market. These programs facilitated the widespread adoption of the 30 year mortgage, making it easier for individuals to access home financing.

1960s-1980s: The Golden Age of the 30 Year Mortgage

The post-war economic boom witnessed a surge in homeownership, fueled by the affordability and stability of the 30 year mortgage. During this period, interest rates remained relatively low, making monthly payments manageable for many borrowers. This era also saw the development of the secondary mortgage market, allowing lenders to sell mortgages to investors, further increasing the availability of financing.

1990s-2000s: The Rise and Fall of Subprime Mortgages

The late 20th century saw a shift towards more complex mortgage products, including adjustable-rate mortgages (ARMs) and subprime mortgages. While these options initially offered lower initial payments, they also carried higher risks, particularly during periods of rising interest rates. The housing bubble of the 2000s, fueled by lax lending standards and subprime mortgages, ultimately led to the financial crisis of 2008.

2010s-Present: The Era of Refinancing and Low Rates

The aftermath of the financial crisis saw a significant tightening of lending standards and a renewed focus on responsible lending practices. Interest rates remained at historically low levels, creating opportunities for borrowers to refinance existing mortgages at lower rates. This period also witnessed the emergence of online mortgage lenders, offering greater transparency and convenience for borrowers.

Current Trends in the 30 Year Mortgage Market

The 30 year mortgage market continues to evolve, reflecting the changing economic landscape, regulatory environment, and consumer preferences.

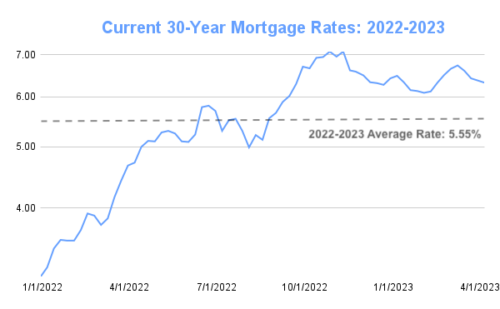

1. Rising Interest Rates:

Since 2022, interest rates have been on an upward trajectory, driven by inflation and the Federal Reserve’s monetary policy tightening. This increase has led to higher monthly payments for borrowers, making homeownership more expensive.

2. The Impact of Inflation:

High inflation has eroded purchasing power, impacting affordability and increasing demand for larger mortgages. This has led to a rise in average loan amounts and a growing concern about mortgage affordability.

3. The Rise of Jumbo Mortgages:

As home prices continue to rise, more borrowers are seeking jumbo mortgages, which are loans exceeding the conforming loan limits set by Fannie Mae and Freddie Mac. These mortgages typically come with higher interest rates and stricter qualifying requirements.

4. The Growing Importance of Credit Scores:

Lenders are placing greater emphasis on credit scores, reflecting the need to mitigate risk in a volatile market. Borrowers with strong credit scores are able to secure better interest rates and more favorable loan terms.

5. Increased Use of Mortgage Technology:

The adoption of digital mortgage platforms and online applications has streamlined the mortgage process, offering greater convenience and transparency for borrowers.

Related Searches and Insights

1. 30 Year Mortgage Rates:

Understanding current 30 year mortgage rates is crucial for borrowers to make informed decisions. Factors influencing rates include the Federal Reserve’s monetary policy, inflation, and overall economic conditions. Market trends, economic forecasts, and expert opinions can provide valuable insights into future rate movements.

2. 30 Year Mortgage Calculator:

Mortgage calculators are essential tools for borrowers to estimate monthly payments, total interest paid, and affordability based on loan amount, interest rate, and loan term. Online calculators offer flexibility and allow borrowers to explore various scenarios and compare different loan options.

3. 30 Year Mortgage vs. 15 Year Mortgage:

Choosing between a 30 year mortgage and a 15 year mortgage depends on individual financial goals and risk tolerance. A 30 year mortgage offers lower monthly payments, while a 15 year mortgage results in faster equity building and lower overall interest costs.

4. 30 Year Mortgage Requirements:

Understanding the eligibility requirements for a 30 year mortgage is essential for borrowers to assess their chances of approval. These requirements typically include credit score, debt-to-income ratio, income verification, and down payment.

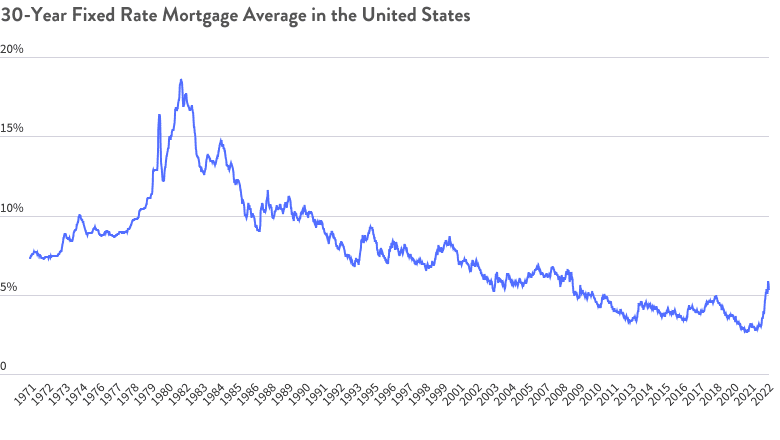

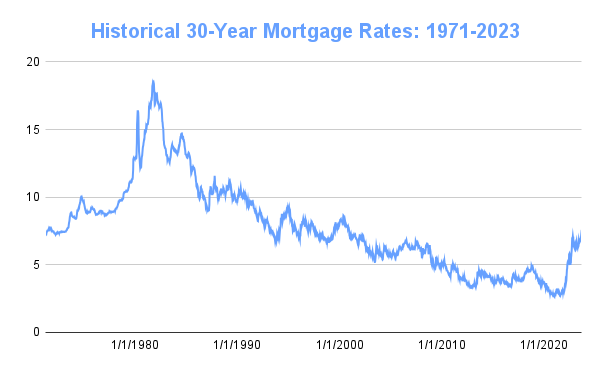

5. 30 Year Mortgage Interest Rates History:

Analyzing historical 30 year mortgage interest rates provides valuable context for current market conditions. Understanding historical trends can help borrowers anticipate potential future rate movements and make informed decisions.

6. 30 Year Mortgage Refinancing:

Refinancing a 30 year mortgage can be beneficial if interest rates have declined, allowing borrowers to lower their monthly payments or shorten the loan term. Understanding refinancing options, eligibility criteria, and potential costs is crucial for making informed decisions.

7. 30 Year Mortgage Prepayment Penalty:

Some lenders may impose prepayment penalties if borrowers pay off their mortgage early. Understanding the terms of the loan agreement and potential penalties is crucial for borrowers considering prepayment strategies.

8. 30 Year Mortgage Loan Fees:

Mortgage loans come with various fees, including origination fees, closing costs, and appraisal fees. Understanding these fees and their impact on the overall cost of borrowing is crucial for borrowers to budget effectively.

Frequently Asked Questions (FAQs) about 30 Year Mortgages

1. What is a 30 year mortgage?

A 30 year mortgage is a type of home loan with a fixed interest rate and a repayment term of 30 years. This long-term financing option offers predictable monthly payments and allows borrowers to build equity over time.

2. What are the benefits of a 30 year mortgage?

The benefits of a 30 year mortgage include:

- Lower Monthly Payments: Compared to shorter-term loans, 30 year mortgages have lower monthly payments, making homeownership more affordable.

- Predictability and Stability: The fixed interest rate provides stability and allows borrowers to budget effectively.

- Longer Term: The 30-year term allows borrowers to spread out their payments over a longer period, reducing the financial burden.

- Equity Building: Consistent monthly payments gradually build equity in the home, providing financial security and potential for future appreciation.

3. What are the drawbacks of a 30 year mortgage?

The drawbacks of a 30 year mortgage include:

- Higher Total Interest Paid: Over the 30-year term, borrowers pay significantly more interest compared to shorter-term loans.

- Longer Repayment Period: It takes longer to pay off the loan, potentially delaying financial goals like retirement planning.

- Interest Rate Risk: While the interest rate is fixed, it may be higher than current rates if refinancing opportunities arise.

4. Who is a 30 year mortgage suitable for?

A 30 year mortgage is suitable for borrowers who:

- Prioritize affordability and lower monthly payments.

- Seek predictable and stable monthly payments.

- Prefer a longer repayment term to manage their financial obligations.

- Aim to build equity gradually over time.

5. How do I qualify for a 30 year mortgage?

Qualifying for a 30 year mortgage typically involves:

- A strong credit score: A score of at least 620 is generally required for conventional loans.

- A low debt-to-income ratio: This measures the percentage of your income dedicated to debt payments.

- A stable income: Lenders require proof of consistent income to ensure repayment ability.

- A sufficient down payment: The minimum down payment for conventional loans is 3%, while FHA loans require a minimum of 3.5%.

6. What are the current 30 year mortgage rates?

Current 30 year mortgage rates fluctuate based on market conditions, economic factors, and lender policies. It is advisable to consult with a mortgage lender or check reputable online resources for the most up-to-date rates.

7. How can I find the best 30 year mortgage rate?

Finding the best 30 year mortgage rate requires comparing offers from multiple lenders, considering factors such as credit score, loan amount, and loan terms. Online mortgage marketplaces and comparison websites can simplify the process and help borrowers identify the most competitive rates.

Tips for Choosing a 30 Year Mortgage

1. Shop Around for Rates: Compare offers from multiple lenders to secure the best possible interest rate and loan terms.

2. Understand Your Credit Score: A strong credit score can significantly improve your chances of approval and secure a lower interest rate.

3. Assess Your Debt-to-Income Ratio: Ensure your debt-to-income ratio is manageable to qualify for a loan and avoid financial strain.

4. Consider Loan Fees: Factor in loan fees, such as origination fees, closing costs, and appraisal fees, when comparing offers.

5. Explore Refinancing Options: If interest rates decline, consider refinancing your mortgage to lower your monthly payments or shorten the loan term.

6. Get Pre-Approved: Obtaining pre-approval from a lender provides confidence in your ability to buy a home and helps streamline the mortgage process.

7. Consult with a Financial Advisor: Seek professional guidance from a financial advisor to develop a comprehensive financial plan that includes mortgage financing.

Conclusion

The 30 year mortgage has played a pivotal role in shaping the American dream of homeownership. Its evolution has been influenced by economic cycles, government policies, and changing consumer preferences. Understanding the historical trends, current dynamics, and future prospects of this essential financial instrument is crucial for borrowers to make informed decisions and navigate the complexities of the housing market. By carefully considering their financial goals, exploring various loan options, and seeking professional guidance, borrowers can leverage the benefits of the 30 year mortgage to achieve their homeownership aspirations.

Closure

Thus, we hope this article has provided valuable insights into The Evolution of the 30 Year Mortgage: A Comprehensive Look at Trends and Insights. We hope you find this article informative and beneficial. See you in our next article!